Vault infrastructure for institutional-grade yield.

Access, deploy and manage onchain vaults. Accessed by Fortune 500 companies, ETP issuers and leading curators.

See everything. Trust nothing blindly.

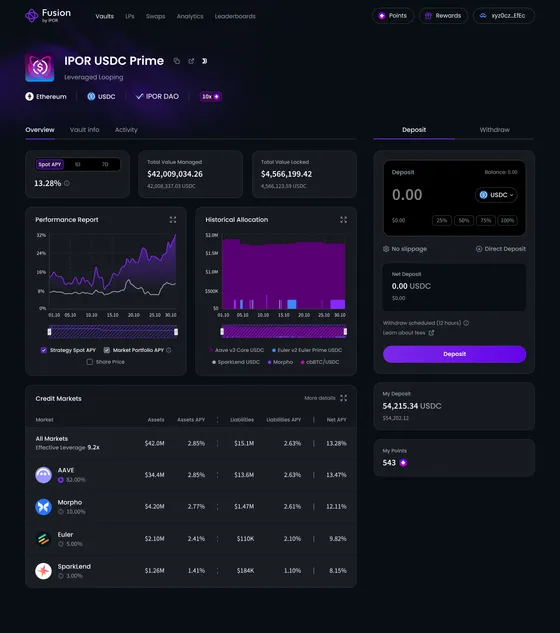

Every vault in Fusion exposes its full mechanics: allocations, performance, costs, and onchain activity. You always know exactly what's happening with your capital.

Real-Time Performance Reports

Historical Allocation Breakdown

Protocol-Level Credit Markets

Live

Yield MetricsLive Yield Metrics

Transaction-Level Auditability

Cost & Slippage Transparency

*Product interface shown for illustrative purposes only. Displayed values are simulated and do not represent actual portfolio performance, balances, or guaranteed returns.

Testimonials

Trusted by the teams building the future of onchain capital.

Leading curators, asset managers and projects rely on Fusion to power their onchain strategies.

“Working with the IPOR Fusion team has been an exceptional experience. They bring a deep level of technical expertise and market understanding, but just as importantly, they are highly collaborative and really great to work with. Throughout our vault build, they have partnered closely with us, showing real commitment to getting the details right and helping us solve complex challenges as they arise. What stands out is their ability to combine strong infrastructure with a practical, delivery-focused mindset. The result is a solution that is not only truly institutional-grade, but also at the forefront of where the market is heading. They have been a key partner in helping us bring our vault vision to life, and couldn’t recommend them more highly.”

“IPOR Fusion drastically reduces our operational overhead, allowing us to launch better vaults, faster. Building directly on Fusion infrastructure, we established the largest cbETH position on the Base network and grew Aave's cbETH market by over 190% in a single month. Their team is always responsive and proactive in helping us optimize our strategies.”

“We have worked closely with the IPOR Fusion team and consistently found them to be responsive, technically rigorous, and thoughtful about risk. They engage seriously with feedback and hold themselves to a high standard, which makes them a reliable team to collaborate with in DeFi.”

“Reservoir has leveraged IPOR Fusion vaults to deliver high-efficiency, leveraged exposure to our yield-bearing stablecoin (wsrUSD) optimizing for liquidity and high returns. Reservoir’s BTC, ETH, and USDC denominated yield vaults offer industry leading risk adjusted yields through automated onchain risk management. IPOR Fusion is robust, user-friendly, and seamless for onchain asset management—making it effortless for partners like us to scale sophisticated strategies with strong risk controls. The IPOR Labs team has been exceptional to work with: responsive, innovative, and deeply aligned on building composable DeFi infrastructure.”

Infrastructure that enforces your edge.

Every component of Fusion is designed for asset managers who need performance, transparency, and composability at institutional scale.

Modular Vault Architecture

Compose strategies from reusable building blocks. Mix lending, staking, and LP positions in a single vault with full atomicity.

Efficient Off-Chain Execution

Alpha engines execute strategy logic off-chain and batch operations onchain through governance-approved parameters, minimizing transaction overhead while maintaining full transparency.

Institutional-Grade Risk Controls

Real-time exposure monitoring, Guardian roles for emergency actions, and configurable market limits ensure capital protection at every layer of the stack.

Multi-Chain Execution

Deploy identical strategies across Ethereum, Arbitrum, Base, and Unichain from a single interface with unified reporting.

Transparent Performance Analytics

On-chain verifiable P&L, historical NAV tracking, and strategy attribution, all visible on the Fusion dashboard and verifiable directly from smart contracts.

Architecture

One vault. Every strategy.

Full control.

Fusion’s modular architecture separates execution from custody. Deploy capital into Fusion Plasma Vaults, connect strategy logic through composable fuses, and let Alpha engines optimize across them, all in a plug & play fashion, fully customizable per strategy needs.

Deposit

Deposit

Morpho

Morpho Aave

Aave Euler

EulerFusion Vaults

ERC-4626 compliant, immutable vaults that hold your assets. Each vault is fully isolated with siloed risk and no cross-contamination. Deposit once, access every integrated market.

Fuse Modules

Composable, non-upgradable smart contract connectors to external protocols. Supply, borrow, swap, loop: each action is a fuse. Snap new ones in, never touch the vault.

Alpha Execution

Off-chain strategy engines execute onchain through governance-approved parameters. Automated rebalancing, carry trades, looping, and arbitrage, all intelligence-driven and risk-bounded.

Solutions

Built for every participant in the vault stack.

Whether you’re allocating treasury capital or building the next yield product, Fusion is the infrastructure layer underneath.

Institutions & Fund Managers

Sovereign vault infrastructure for onchain asset management. Deploy capital with institutional-grade security, full transparency, and customizable risk parameters. Your vault, your rules, your alpha.

- Privacy-preserving strategy execution

- Configurable fee structures & governance

- Python SDK, no Solidity required

- White-label ready for distribution partners

Builders & Curators

Create automated onchain vaults without writing a single smart contract. Pick your fuses, set your parameters, and launch. Earn curator fees from the strategies you design.

- Plug-and-play fuse library

- One-click vault deployment via Factory

- Composable across 20+ protocols

- Earn fees as an Atomist

Liquidity Providers

Access professionally curated, auto-optimized yield strategies with a single deposit. From lending optimization to leveraged looping, risk-adjusted to your preference.

- One-click deposit into curated strategies

- Automated rebalancing & compounding

- Siloed risk, no socialized losses

- Instant liquidity, no lockups

Protocols & Distributors

Embed Fusion vaults as plug-and-play yield products. Wallets, exchanges, and fintechs can offer 'Earn' features powered by Fusion infrastructure without building from scratch.

- Embed vaults into any interface

- White-label for wallets & CEXs

- Referral system built-in

- Invisible infrastructure, visible yield

Plug & Play

40+ onchain protocols and 170 interaction methods, reachable through pre-built fuse modules.

Better by Design

How Fusion Vaults outperform the alternative.

Merkle proof vaults were a first step. Fusion is the leap forward: transparent, composable, and built for speed.

Security

Transparent & battle-tested vault infrastructure.

Immutable vault logic. Non-upgradable fuses. Role-based access control. Fusion is built by engineers from banking, payments, and insurance, and audited by the best in Web3.

Independent security audits

Immutable vault & fuse contracts

Admin keys over depositor funds

Ecosystem News

The latest from the Fusion ecosystem.

Partnerships, integrations and milestones from the teams building institutional-grade onchain yield on Fusion.

Tesseract Selects IPOR Fusion as Onchain Vault Infrastructure for Institutional Clients

Tesseract Investment Oy, a Helsinki-based MiCA-authorised CASP, has selected Fusion as its onchain vault infrastructure for institutional onchain yield, with 21Shares among the launch partners.

BitGo Opens Institutional Access to Tesseract's Dedicated Client Vaults Powered by Fusion

Eligible institutions can now allocate to Tesseract's Dedicated Client Vaults, powered by Fusion, directly from BitGo qualified custody, with assets staying inside the custodial perimeter.

The Vault layer is ready.

Deploy your first vault, deposit into a curated strategy, or embed Fusion into your product.